Fiscal policies in Austria during the Covid-19 pandemic

A macroeconomic assessment

Author: Klaus Weyerstraß

When the new corona virus SARS-CoV-2 began to spread rapidly in Austria, the government reacted with the first lockdown, beginning on March 16th, 2020. This blog posts examines the overall macroeconomic impacts of the measures taken to counteract the consequences of the pandemic.

From the start of the pandemic, extensive fiscal policy support measures were adopted, aiming at cushioning the economic impact of the disruptions in global supply chains, declining external demand, and the containment measures. As further lockdowns became necessary during new Coronavirus waves, the government extended parts of the measures in November 2020 and in spring 2021.

On the expenditure side of the government budget, the policy packages consist of:

- a short-term work scheme, the foundation of the Corona labour foundation (Kurzarbeit, Corona-Arbeitsstiftung),

- a hardship fund (Härtefallfonds),

- fixed cost grant to businesses that lost sales (Fixkostenzuschuss),

- turnover compensation (Umsatzersatz),

- Fund for NPOs including sports leagues, higher unemployment benefits for long-term unemployed, a one-off child benefit,

- and an investment premium (Investitionsprämie).

On the revenue side, measures include an

- Income tax reform,

- the temporary reduction of value added tax (VAT) rates for hotels and restaurants as well as the publication and cultural sector,

- a loss carryback,

- the introduction of a temporary degressive depreciation for investment,

- tax deferrals and reduced tax prepayments.

Furthermore, the government assumed liability for loans granted by banks to companies. In addition, the packages comprised co-financing by the central government of to 50% of the costs involved in local investment programs with a particular focus on green investment and public spending on digitalisation of education, public transport, and subsidies to companies for investments in climate-friendly innovations and industries. Details on the fiscal policy measures can be found in Prammer (2020) and in Budgetdienst (2021). The latter publication contains also the most recent update of the figures which are continuously updated in view of the actual uptake of the budgeted funds.

In the autumn of 2020, the Austrian Ministry of Finance commissioned a macroeconomic assessment of the fiscal policy measures from research institutes WIFO (Österreichisches Wirtschaftsforschungsintitut - Austrian Institute of Economic Research) and IHS (Institut für Höhere Studien - Institute for Advanced Studies). Parts of the measures, in particular the distributional and labour supply effects of the income tax reduction, were evaluated by the WIFO with a microsimulation model. Both WIFO and IHS used their respective macroeconometric models to assess the overall macroeconomic impacts of the measures. Detailed results of the evaluation can be found in Baumgartner et al. (2020). In Weyerstrass (2021), results obtained with the IHS macroeconomic model are described in detail along with details on the macroeconometric model LIMA. This blog post summarises the main findings of the latter paper.

Results

For the evaluation of the effect of the fiscal policies, the IHS economic forecast from October 2020 was used as a baseline and compared with a counterfactual situation without public measures. The deviations from the baseline simulation measure the macroeconomic impulses the fiscal policy measures.

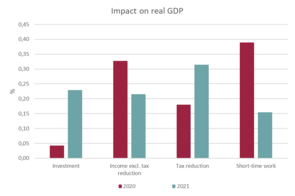

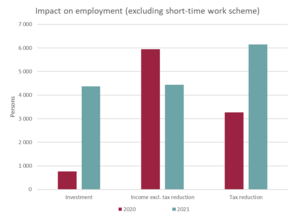

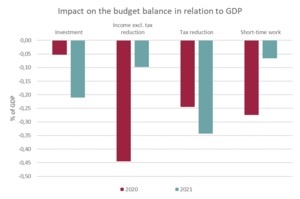

The tax reduction raises real consumption by 0.4 percent in 2020 and by 0.6 percent in 2021. Real GDP is higher by 0.2 percent and 0.3 percent, respectively. Employment is expected to be about 3,300 (2020) and about 6,150 (2021) persons higher than without implementation of the tax reform. In 2021, public debt will be about 2.5 billion euro higher than without the tax reduction, leading to an increase of 0.34 percentage points in the budget balance ratio.

The measures aimed at increasing disposable income of private households excluding the tax reduction raise real GDP by 0.33 percent in 2020 and by 0.22 percent in 2021. The number of employees is higher by around 6,000 persons in 2020 and by slightly less than 4,500 persons in 2021. This decreases the unemployment rate by 0.09 and 0.03 percentage points, respectively. The measures worsen the budget balance by around 0.5 percent of GDP in 2020 and by 0.1 percent of GDP in 2021. The impact on inflation is negligible because of a strong underutilisation of production capacities in particular in spring and summer 2020. The increase in production leads to higher labour demand, while the effect on wages is negligible due to high unemployment. The (slight) increase in employment and (very small) nominal wage increases lead to an expansion of the wage bill and a further increase in disposable income of private households.

Taking all measures together, both in 2020 and in 2021 real GDP was by about 0.9 percent higher than without this fiscal policy support.

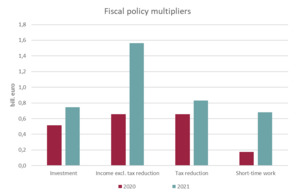

For the investment premium, an additional investment impulse of 200 million euro in 2020 and 700 million euro in 2021 was assumed on impact, whereby cumulatively only € 400 million represent a real additional impulse. Since the premium was only temporarily granted in 2020 and 2021, it was assumed that investments of around €500 million already planned for 2022 would be brought forward in order to benefit from the subsidy. According to the simulation results, the investment premium and the temporary degressive depreciation raise gross fixed capital formation by 0.4 percent in 2020 and by 1.6 percent in 2021. Via multiplier effects, also private consumption is positively affected. Since also imports rise, the overall impact on GDP is dampened. According to the model simulations, GDP is higher by 0.04 percent in 2020 and by 0.23 percent in 2021. Higher investment has a short-term demand effect. In the medium to long term, productivity is raised by the increase in the capital stock and the implementation of new technologies. Both measures primarily cause investments to be brought forward from subsequent years, which will thus lead to weaker investment activity from 2022 onwards. The main budget burden also lies outside the analysis horizon after 2021.

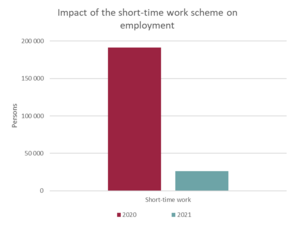

According to results from the micro simulation which were also part of the overall study by Baumartner et at. (2020), the short-time work scheme stabilises employment by 184,000 persons. This number was used as an exogenous input for the model simulations. Due to multiplier effects, the overall employment effect amounts to about 191,000 employees in 2020. The number of unemployed persons is by 153,000 lower than without this measure, and the unemployment rate is reduced by 3.8 percentage points. Real GDP is by about 0.4 percent higher in 2020. Due to carry-over effects, also in 2021 GDP and employment are higher than without this measure. The budget balance deteriorates by about 1.2 percent of GDP in 2020 and by slightly less than 0.1 percentage points in 2021.

Taking all measures together, both in 2020 and in 2021 real GDP was by about 0.9 percent higher than without this fiscal policy support. Employment was higher by about 200,000 persons in 2020 and by 41,000 employees in 2021. The public budget deteriorated by 8.3 billion euro in 2020 and 3.2 billion euro in 2021, implying that the deficit ratio was about 2 percentage points higher in 2020 and by about 0.75 percentage points in 2021 as compared to a counterfactual situation without the fiscal policy support. As real GDP slumped by around 7 percent in 2020, the measures were suitable to cushion the decline, but due to the severity of the crisis the slump could only be mitigated somewhat. Since most of the measures were aimed at supporting disposable income of private households, the estimated effect on private consumption is much stronger than on GDP. Investment also decreased less than it would otherwise have been the case, but especially due the time limit of the investment premium and of the degressive depreciation, the measures affect mainly the temporal profile and less the absolute level of investment in the coming years.

Summary and conclusions

The Covid-19 pandemic and the measures undertaken to contain its spread led to an historic slump of economic activity. In Austria, the decline of real GDP was much larger than that in the financial crisis of 2008/2009. In particular the speed of the slump in the second quarter of 2020 was unprecedented. As in almost all industrialised and many emerging market economies, the Austrian government announced large fiscal policy measures to cushion the economic impact of the lockdown measures. Relatively high multipliers resulted from the measures aimed at stabilising disposable income of private households. Particularly successful in preventing employment from plummeting in line with real activity was the short-time work scheme.

In a situation in which the recession is not caused by a lack in demand but by government measures to restrict consumption possibilities, support to private consumption is not the recommended fiscal policy reaction. However, support to those employees and self-employed who are affected by closures of some businesses are appropriate. In addition, both to support income and to help companies in maintaining their human capital, the short-time work scheme is an appropriate measure. However, while noting that such a distinction is difficult in practice, it is important that those companies that would have left the market anyway should not be kept alive artificially. This would hamper structural change. For the same reason, short-time work schemes should only be offered as long as the containment measures or other pandemic-related problems such as supply-chain disruptions prevail.

As soon as the immediate macroeconomic impacts of the pandemic are overcome, the sustainability of public finances must be restored. In the medium-term future, public finances will come under pressure due to population ageing, resulting in lower public revenues and higher expenditures for pensions and long-term care. In addition, the digitalisation of the economy and fighting climate change will require public investment. Hence, pandemic-related policies must be removed as soon as the economic situation makes it possible.

References

Baumgartner, J., Fink, M., Lappöhn, S., Moreau, C., Plank, K., Rocha-Akis, S., Schnabl, A., Weyerstrass, K. (2020), Wirtschaftspolitische Maßnahmen zur Abfederung der COVID-19-Krise. Mikro- und makroökonomische Analysen zur konjunkturellen, fiskalischen und verteilungspolitischen Wirkung. Joint IHS and WIFO study, commissioned by the Austrian Ministry of Finance.

Budgetdienst (2021), COVID-19-Berichterstattung. Vollzug 2020 und Ausblick 2021. https://www.parlament.gv.at/ZUSD/BUDGET/2021/BD_-_COVID-19-Berichterstattung_Vollzug_2020_und_Ausblick_2021_BF.pdf (18 October 2021).

Prammer, D. (2021), Unprecedented fiscal (re)actions to ease the impact of the COVID-19 pandemic in Austria, Monetary Policy & the Economy, Oesterreichische Nationalbank (Austrian Central Bank), issue Q4/20-Q1/, 153-173.